Picture this: You’re a second-year engineering student at a prestigious college in Bangalore, watching your seniors effortlessly book movie tickets online, shop during flash sales, and even earn cashback on their purchases. Meanwhile, you’re still asking your parents for money every time you want to buy something online or need cash for unexpected expenses.

This scenario plays out in thousands of Indian households every day. As a student without a steady income, getting a credit card might seem impossible – but it’s not. The Indian banking sector has evolved significantly, and several banks now offer student-friendly credit cards designed specifically for people in your situation.

I’ve spent considerable time researching and analyzing the current credit card landscape for students in India, and I’m excited to share insights that could help you start building your financial future today. The best part? You don’t need a hefty salary slip or income proof to get started.

Why Indian Students Need Credit Cards More Than Ever

The digital revolution has transformed how we handle money in India. From UPI payments to online shopping, digital transactions have become the norm rather than the exception. However, many financial opportunities still require a credit history – something most students lack.

Here’s what’s happening in the Indian student financial landscape:

The Changing Payment Ecosystem

Digital-First Approach: With over 74% of Indian consumers preferring digital payments post-COVID, students without credit cards often miss out on exclusive online deals, cashback offers, and instant EMI options.

E-commerce Growth: India’s e-commerce market is expected to reach $350 billion by 2030. Students without credit cards cannot access many platform-specific offers, early access sales, or build-your-own-EMI options.

Early Credit Building Advantages

Starting your credit journey as a student in India offers several long-term benefits:

Lower Interest Rates: A good credit score established early can save you lakhs in interest when you apply for personal loans, home loans, or car loans after graduation.

Employment Opportunities: Many multinational companies and financial institutions in India now check credit scores as part of their hiring process, especially for finance and management roles.

Rental Applications: In metro cities like Mumbai, Delhi, and Bangalore, landlords increasingly ask for credit score verification, especially for premium properties.

Understanding Student Credit Cards in the Indian Context

Unlike Western countries where student credit cards are commonplace, India’s regulatory environment has been more conservative. However, the Reserve Bank of India (RBI) has gradually relaxed norms, making it easier for students to access credit products.

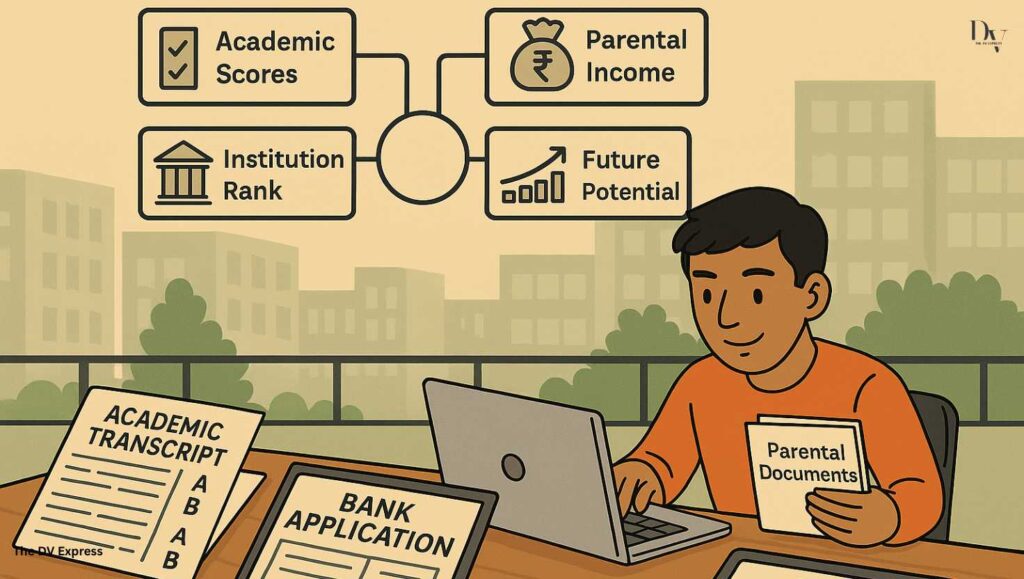

How Indian Banks Assess Student Credit Applications

Indian banks have developed unique assessment criteria for student credit cards:

Educational Institution Ranking: Banks often have tie-ups with premier institutions like IITs, IIMs, NITs, and leading private universities. Students from these institutions may get preferential treatment.

Academic Performance: Some banks consider your academic scores, with higher marks potentially leading to better credit limits or terms.

Parental Income: While you might not have income, your parents’ financial stability often plays a crucial role in approval decisions.

Future Earning Potential: Banks assess your course and potential future earnings. Engineering, medicine, and MBA students often get better offers than those in other fields.

Top Student Credit Cards Available in India (2025 Updated)

Let me walk you through the best options currently available for students with no income:

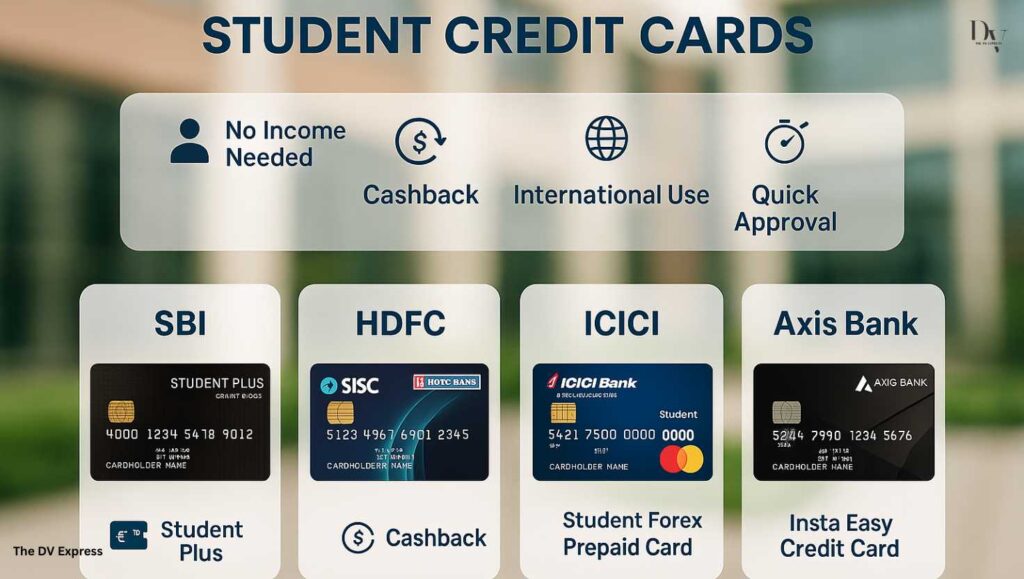

1. SBI Student Plus Advantage Card – The Beginner’s Best Friend

State Bank of India, being the largest public sector bank, offers one of the most accessible student credit cards in India.

Key Features:

- No Income Requirement: Perfect for students with zero income

- Low Credit Limit: Starts from ₹10,000 to ₹50,000 based on profile

- Lifetime Free: No annual fees throughout the card’s validity

- Parental Guarantee: Parents can act as guarantors without additional documentation

- Easy Approval: High approval rates for students from recognized institutions

Eligibility Criteria:

- Must be enrolled in a recognized college/university

- Age between 18-25 years

- Parents should have a good credit history

- Valid student ID and college admission letter required

Real-World Benefit: I know several students who got approved for this card within a week of application, even with zero credit history.

2. HDFC Bank Student Credit Card – Premium Features for Deserving Students

HDFC Bank’s student offering caters to students from premier institutions with excellent features.

Key Features:

- Reward Points: Earn 2 reward points for every ₹150 spent

- Fuel Surcharge Waiver: 1% fuel surcharge waiver at all petrol pumps

- Dining Offers: Up to 25% discount at partner restaurants

- Online Shopping Benefits: Additional cashback on select e-commerce platforms

- International Usage: Can be used abroad with reasonable forex rates

Eligibility Requirements:

- Student of recognized university/college

- Must have an HDFC Bank savings account

- Parents’ income documentation required

- Age between 18-25 years

Strategic Advantage: This card helps students build a relationship with HDFC Bank, which can be beneficial for future financial products.

3. ICICI Bank Student Forex Prepaid Card – Perfect for Study Abroad Dreams

While technically not a credit card, ICICI’s student forex card bridges the gap for international students.

Key Features:

- Multi-Currency Support: Load up to 15 currencies

- Study Abroad Benefits: Special rates for education-related expenses

- Parental Control: Parents can reload and monitor expenses

- Emergency Cash: 24/7 emergency cash assistance globally

- Online Management: Easy online account management and tracking

Ideal For: Students planning to study abroad or those frequently traveling internationally.

4. Axis Bank Insta Easy Credit Card – The Quick Approval Option

Axis Bank’s digital-first approach makes this card attractive for tech-savvy students.

Key Features:

- Instant Approval: Digital approval process within minutes

- Flexible Credit Limit: ₹10,000 to ₹1,00,000 based on profile

- Contactless Payments: Tap and pay functionality

- Mobile App Integration: Seamless mobile banking integration

- Student Discounts: Partnerships with various student-focused merchants

Application Process: Completely online with minimal documentation required.

Secured Credit Cards: Your Stepping Stone to Financial Independence

If you’re struggling to get approved for traditional student credit cards, secured credit cards offer an excellent alternative.

How Secured Credit Cards Work in India

Security Deposit System: You deposit an amount (typically ₹10,000 to ₹50,000) with the bank, which becomes your credit limit. This deposit acts as collateral, reducing the bank’s risk.

Credit Building Mechanism: Your payment history is reported to credit bureaus (CIBIL, Experian, etc.), helping you build a credit score from scratch.

Graduation Opportunity: After 6-12 months of good payment history, many banks convert secured cards to unsecured ones and return your deposit.

Top Secured Credit Card Options

1. SBI Secured Credit Card

- Minimum deposit: ₹25,000

- Credit limit: 85% of deposit amount

- Annual fee: ₹499 (waived for first year)

- Good for building initial credit history

2. HDFC Millennia Secured Credit Card

- Minimum deposit: ₹25,000

- Rewards on online shopping and bill payments

- Annual fee: ₹1,000 (can be waived based on spending)

- Premium card benefits even with secured nature

Strategic Insight: Many successful professionals I know started their credit journey with secured cards during their college years. The key is consistency in payments and gradually building trust with the banking system.

Alternative Routes: Add-On Cards and Family Banking

Add-On Credit Cards – Leveraging Family Credit

Many Indian families successfully use add-on cards to help students build credit while maintaining parental oversight.

How It Works:

- Parents apply for an add-on card on their existing credit card

- Student gets a card with their name but linked to parent’s account

- Parents can set spending limits and monitor transactions

- Student’s usage may help build their credit profile

Advantages:

- Immediate access to credit facilities

- Parental guidance and control

- Often no additional fees

- Can help establish credit history

Top Add-On Card Options:

- HDFC Bank Regalia Add-On: Premium benefits with parental oversight

- SBI Simply Click Add-On: Good for online shopping with rewards

- ICICI Bank Coral Add-On: Balanced features for students

Family Banking Relationships

Building a strong relationship with your family’s primary bank can significantly improve your chances of getting a student credit card.

Strategies That Work:

- Open a salary account with the bank (if you have any part-time income)

- Maintain a good balance in your savings account

- Use the bank’s other services (insurance, investments)

- Ensure your parents have a good relationship with the bank

Building Credit Responsibly: The Indian Student’s Guide

Getting a credit card is just the first step. Using it responsibly is what sets you up for long-term financial success.

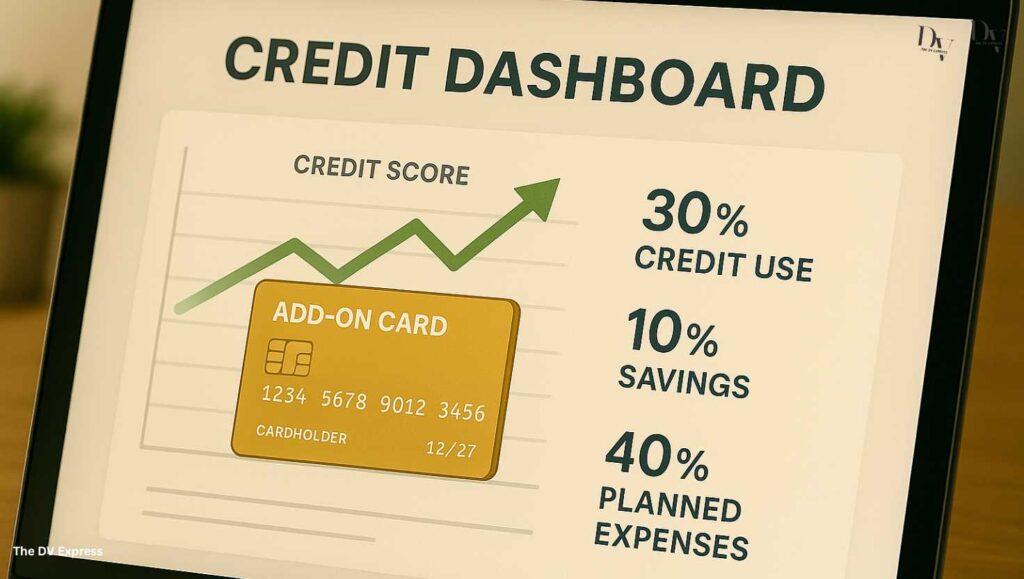

The 30-10-40 Rule for Indian Students

I recommend following a modified version of international credit best practices, adapted for Indian students:

30% Rule: Never use more than 30% of your credit limit. If your limit is ₹20,000, don’t spend more than ₹6,000 in a month.

10% Savings Rule: Save at least 10% of any money you receive (pocket money, part-time earnings) specifically for credit card payments.

40% Planning Rule: Plan at least 40% of your credit card usage for essential expenses like books, stationery, or emergency situations.

Smart Usage Strategies for Students

1. Automate Your Payments Set up automatic payments for at least the minimum amount due. This ensures you never miss a payment, which is crucial for building a good credit score.

2. Use Credit Cards for Planned Expenses Don’t use your credit card for impulse purchases. Plan your expenses and use the card strategically for things you would have bought anyway.

3. Take Advantage of Student Offers Many credit cards offer special discounts for students on:

- Educational software and subscriptions

- Online courses and certifications

- Books and stationery

- Food delivery and transportation

Digital Payment Integration and UPI Compatibility

The rise of UPI has revolutionized payments in India, and modern credit cards seamlessly integrate with this ecosystem.

Credit Card UPI Integration

RuPay Credit Cards: Many banks now offer RuPay credit cards that work directly with UPI, allowing you to use credit for UPI payments.

Benefits for Students:

- Pay for small expenses using credit through UPI

- Earn rewards on everyday spending

- Better expense tracking through UPI transaction history

- Access to UPI-specific offers and cashback

Popular Apps and Integration

Google Pay: Link your credit card for seamless payments PhonePe: Excellent integration with various bank credit cards Paytm: Good for bill payments and recharges using credit cards Amazon Pay: Useful for students who shop frequently on Amazon

Common Mistakes Indian Students Make with Credit Cards

Through my research and interactions with financial advisors, I’ve identified several pitfalls that Indian students commonly encounter:

1. The “Free Money” Misconception

Many students treat credit cards as free money rather than borrowed money. This leads to overspending and debt accumulation.

Reality Check: Every rupee you spend on a credit card needs to be repaid with interest if not paid on time. The interest rates in India typically range from 36-48% annually.

2. Ignoring Due Dates

Missing payment due dates can severely impact your credit score and lead to penalty charges.

Solution: Set multiple reminders on your phone and consider automatic payments for at least the minimum amount due.

3. Cash Advance Usage

Using credit cards for cash withdrawals comes with high fees and immediate interest charges.

Better Alternative: Plan your cash needs in advance and withdraw from your savings account or ask family for support.

4. Applying for Multiple Cards

Students often apply for multiple credit cards simultaneously, which can negatively impact their credit score.

Recommended Approach: Start with one card, use it responsibly for 6-12 months, then consider additional cards if needed.

Expert Tips for Maximizing Student Credit Card Benefits

Seasonal Shopping Strategies

Festival Season Benefits: During festivals like Diwali, Dussehra, and regional celebrations, credit cards offer enhanced rewards and discounts. Plan your purchases during these periods to maximize benefits.

Back-to-School Offers: Many cards provide special discounts on educational materials, laptops, and software during the academic year’s beginning.

Building Long-term Banking Relationships

Consistency is Key: Stick with one bank for multiple services. This relationship building can lead to better offers and easier approvals for future financial products.

Regular Usage: Use your card regularly but responsibly. Banks prefer customers who use their cards consistently over those who keep them idle.

The Future of Student Credit Cards in India

The Indian financial landscape is rapidly evolving, and student credit cards are becoming more sophisticated and accessible.

Emerging Trends

AI-Powered Credit Assessment: Banks are using artificial intelligence to assess creditworthiness beyond traditional metrics, potentially making approval easier for students.

Embedded Finance: Credit cards are being integrated into various platforms, from e-commerce sites to educational apps, providing seamless credit access.

Green Credit Cards: Some banks are introducing environmentally friendly credit cards with special rewards for sustainable spending.

Regulatory Changes

The RBI continues to refine regulations around student lending, potentially making credit more accessible while maintaining consumer protection.

Preparing for Life After Graduation

Your student credit card is just the beginning of your financial journey. Here’s how to prepare for the transition:

Building a Strong Credit Foundation

Maintain Good Payment History: Your payment history during college will impact your ability to get loans and better credit cards after graduation.

Gradually Increase Credit Limits: As you build a history, request credit limit increases to improve your credit utilization ratio.

Diversify Credit Types: After graduation, consider adding a personal loan or other credit products to diversify your credit portfolio.

Transitioning to Regular Credit Cards

Most banks offer attractive upgrade options for students transitioning to regular employment:

Salary Account Benefits: Opening a salary account with the same bank can lead to pre-approved credit card offers with better features.

Career-Specific Cards: Many banks offer specialized cards for different professions (doctors, engineers, CAs) with relevant benefits.

Technology and Security Considerations

As a digitally native generation, Indian students must be aware of credit card security in the digital age.

Digital Security Best Practices

Two-Factor Authentication: Always enable 2FA for your credit card accounts and mobile banking.

Regular Monitoring: Check your credit card statements regularly through mobile apps or SMS alerts.

Secure Networks: Avoid using credit cards on public Wi-Fi networks for online transactions.

Emerging Payment Technologies

Contactless Payments: Most new credit cards come with contactless payment capabilities, perfect for quick transactions.

Biometric Authentication: Some premium cards now offer fingerprint or facial recognition for enhanced security.

Addressing Parental Concerns

Many Indian parents are hesitant about their children getting credit cards. Here’s how to address common concerns:

Building Trust Through Transparency

Open Communication: Discuss your financial goals and how a credit card fits into your plans.

Shared Monitoring: Many banks allow parents to receive SMS alerts for transactions, providing peace of mind.

Educational Approach: Show your parents that you understand the responsibilities and risks involved.

Demonstrating Financial Maturity

Budget Tracking: Maintain a detailed budget and show how a credit card fits into your financial planning.

Emergency Fund: Demonstrate that you have some savings for emergencies, showing you won’t rely solely on credit.

Frequently Asked Questions

Can I get a credit card as a student with no income in India?

Yes, several Indian banks offer student credit cards specifically designed for students with no income. Banks like SBI, HDFC, and ICICI have special programs that consider your educational background, parental support, and future earning potential rather than current income.

What documents do I need to apply for a student credit card?

Typically, you’ll need:

- Valid student ID and college admission letter

- Identity proof (Aadhaar, passport, or driver’s license)

- Address proof

- Parents’ income documents (salary slips or ITR)

- Bank statements (if you have a savings account)

- Academic transcripts (some banks require this)

How does a student credit card affect my CIBIL score?

A student credit card can positively impact your CIBIL score if used responsibly. Timely payments and low credit utilization will help build a strong credit history. However, missed payments or high utilization can negatively affect your score.

Can I use a student credit card for international transactions?

Most student credit cards in India support international transactions, but they may charge foreign exchange fees (typically 2-4%). If you frequently make international payments, look for cards with lower forex fees or consider forex prepaid cards.

What happens to my student credit card after graduation?

Most banks automatically convert student credit cards to regular credit cards after graduation. Your credit limit may be reassessed based on your employment status and income. Some banks offer attractive upgrade options with better features for fresh graduates.

How can I increase my credit limit as a student?

To increase your credit limit:

- Maintain a good payment history for at least 6 months

- Use your card regularly but keep utilization below 30%

- Update your income information if you start earning

- Request a credit limit increase through your bank’s app or customer service

- Provide additional documentation if required

Are there any special offers for students from premier institutions?

Yes, banks often have tie-ups with premier institutions like IITs, IIMs, and NITs, offering better terms, higher credit limits, or special benefits for students from these colleges. Check with your college’s finance office for any banking partnerships.

Conclusion: Your Financial Future Starts Today

Getting your first credit card as a student in India is more than just accessing credit – it’s about taking the first step toward financial independence and building a foundation for your future financial success.

The landscape has never been more favorable for students. With banks recognizing the potential of India’s youth demographic and the RBI’s supportive regulatory environment, options are more accessible than ever before.

Remember, the key to success with student credit cards lies not just in getting approved, but in using them wisely. Start small, pay on time, and gradually build your financial reputation. The habits you develop today will serve you well throughout your career.

Whether you choose a traditional bank card, opt for a secured card, or start with an add-on card through your family, the important thing is to begin your credit journey responsibly. Your future self – the one applying for that dream job, buying that first car, or getting that home loan – will thank you for the strong financial foundation you’re building today.

Take Action Today: Research the options that best fit your situation, gather the necessary documents, and take the first step toward your financial future. Every successful financial journey begins with a single step, and for many Indian students, that step is their first credit card.

About the Author:

Divyanshita Singh is a practicing Chartered Accountant and SEBI Registered Investment Advisor with 5+ years of experience in personal finance and investment planning. She has guided 200+ clients and managed portfolios worth over ₹2 crores. [Read full bio →]